Education is the

most powerful weapon for a modern changing world and our children are the

sparks which will ignite the positive change. Decades of insisting on

children’s education and finally having an increase in the literacy rate has

managed to pave way for brighter and a more innovative generation. Every

metropolitan city is like a race track and every child an athlete. All they

have to do is keep running, cross hurdles and manage to secure a worthy place

in this world. While a child is running the race, a parent will work all their

might to make this journey a comfortable one for their children. From sending

them to the best schools, private institutions, paying for competitive exams,

crash courses and the list is endless. While education is a basic necessity it

comes for a substantial cost, best institutions are a real deal with lakhs of

rupees just being spent over them.

The stress however, is a problem the parents take upon themselves. School education is normally financed by one’s

regular monthly income. Saving for your child’s higher education is what

requires more attention. While arriving at this target, take into account cost

escalations in the future. So if the graduation needs are around Rs.6 lakhs

today, then for a child who is currently three-months-old, after factoring in

the cost escalation (at an average inflation rate of 8 per cent), the amount

required will be around Rs. 24 lakhs, after 18 years.

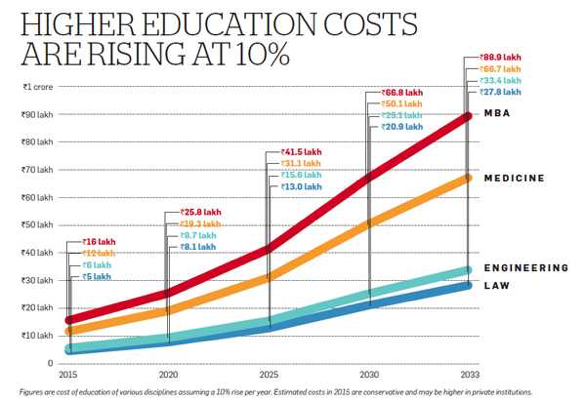

The class of 2018 of the Indian Institute of Management-Ahmedabad will pay Rs

19.5 lakh for the two-year course. This is 400% higher than what the premier business schools

charged in 2007. If the fees of the two-year management course continue to rise

by an average 20% every year, it will cost roughly Rs 95 lakh in 2025.

At this rate, saving for your children’s education once they are in their

teenage years will be a mistake. Starting early gives you the time to invest

little at a time and yet generate enough cash for your children by the time

they reach their graduation schools. The benefits of an early start cannot be

stressed enough when you are saving for a long-term goal. If your child is 3-4

years old, you have a good 13-14 years to save. Starting early

helps you amass larger sums that may not be possible later in life

.

INVESTMENT OPTIONS:

Saving early gives you various investment options which allow you to save for your

child’s education. If you are 30-years-old when you begin saving for your

child, then you can park 60 per cent of your saving in equity and

equity related instruments while the remaining can be in debt and

fixed income instruments.

A good example of a secure investment option for higher

education is PPF. A disciplined year-on-year investment of Rs. 20,000 in to the

PPF account can yield Rs. 5.86 lakhs at the end of 15 years, a good amount to

save if initiated at the time of birth of your child.

For the debt portion, start a recurring deposit that would

mature around the time your child is scheduled to apply for college. If you are

in the highest 30% tax bracket, avoid recurring deposits and start an SIP in a

short-term debt fund. These funds will give nearly the same returns as fixed deposits but are

more tax efficient if the holding period is over three years. If you plan

on investing in insure policies make sure you start out early for low premium

risks and also to ensure higher return by the time your child reaches the age

of 21-22.

Your child is

your responsibility and eventually you will become theirs. Education is the

foundation for your child’s future. Investing in them from the start will yield

more results and less stress towards the end. The result truly starts with you.

The choices need to be smart and the result, effective. Make sure you choose

the right option.

Comments

Post a Comment